Energy Markets

Oil prices fall to $67.39 as easing geopolitical tensions limit supply disruption risks

Oil prices edged lower on Friday and were heading for a second consecutive weekly loss as easing concerns over a potential U.S.-Iran conflict reduced fears of supply disruptions.

As of 5:30 GMT, Brent crude futures slipped 13 cents or 0.19 percent to $67.39 a barrel, after declining 2.7 percent in the previous session. Meanwhile, U.S. West Texas Intermediate (WTI) crude fell 17 cents or 0.27 percent to $62.67, following a 2.8 percent drop on Thursday.

For the week, Brent was on track to lose about 0.8 percent, while WTI was set to decline roughly 1.1 percent.

U.S. could reach deal with Tehran within the next month

Oil prices had risen earlier in the week amid fears that the United States might launch an attack on major Middle Eastern producer Iran over its nuclear program. However, remarks on Thursday from U.S. President Donald Trump suggesting Washington could reach a deal with Tehran within the next month weighed on the market and pushed prices lower in the previous session.

Beyond easing tensions with Iran, the International Energy Agency said in its monthly report on Thursday that global oil demand growth this year is expected to be weaker than previously forecast, with overall supply projected to outpace demand. The report revealed that the global market could face a surplus of just over 3.7 million barrels per day in 2026, highlighting a significant supply glut.

Thursday’s losses were exacerbated by data released earlier showing a sharp surge in U.S. crude inventories, alongside mounting expectations that additional Venezuelan barrels could soon re-enter the market. The Energy Information Administration reported that stockpiles rose by 8.5 million barrels to 428.8 million barrels last week, far surpassing analysts’ expectations of a build of just 793,000 barrels.

Venezuelan output to grow further

Oil prices dropped further amid expectations that Venezuelan output will recover to pre-sanctions levels in the coming months, climbing from around 880,000 barrels per day to roughly 1.2 million bpd. A White House energy official noted on Thursday that the U.S. Treasury is set to grant further authorizations this week to ease sanctions on Venezuela’s energy sector.

U.S. Energy Secretary Chris Wright added that oil sales from Venezuela under U.S. control have generated more than $1 billion since President Nicolas Maduro’s capture in January, with a further $5 billion in revenue anticipated over the next few months.

Investors also stayed on the sidelines ahead of the U.S. consumer price index (CPI) report due later on Friday, which may provide clearer signals on the Federal Reserve’s next policy steps. Robust January employment data released earlier this month has already dampened expectations for imminent interest rate cuts.

Related Articles

Renewable Energy Storage Market 2025 Forecast - La...

21 Oct, 2025 07:12

Solar power mistake in South Africa costs homeowne...

21 Oct, 2025 07:54

An Investor’s Guide to Africa...

21 Oct, 2025 09:47

Doha Strike Shakes Global Energy Assumptions...

22 Oct, 2025 13:01

GCC and Russia Deepening ties in a multipolar Midd...

23 Oct, 2025 11:59

Tesla prepares first steps into Africa with Morocc...

23 Oct, 2025 13:29

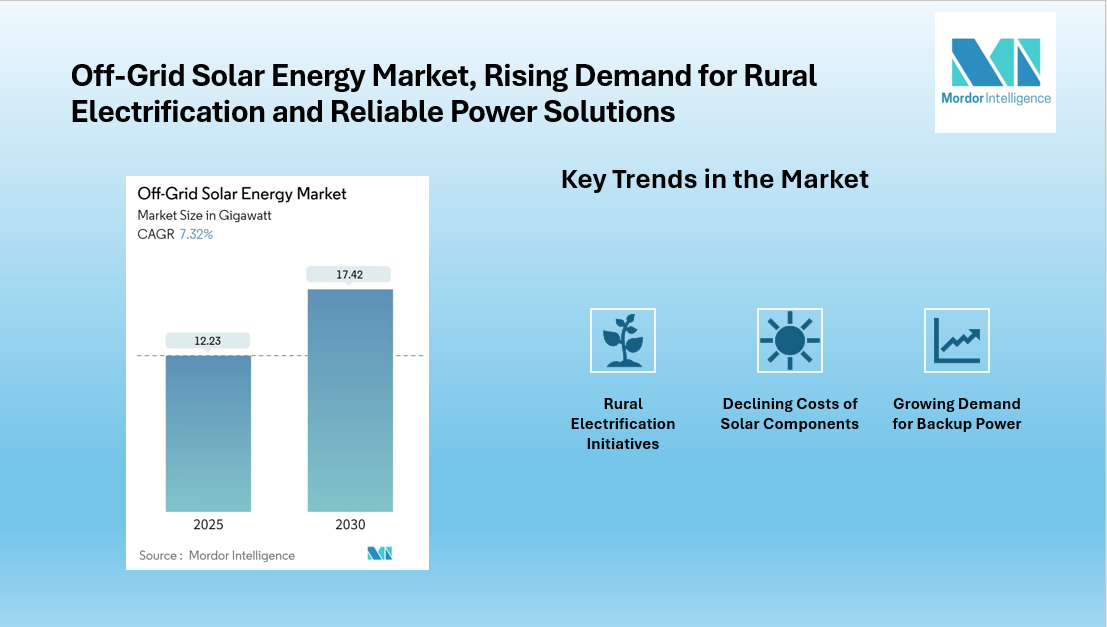

Off-Grid Solar Energy Market to grow at 17.42 GW b...

23 Oct, 2025 13:39

Petroleum Institute Urges Early Take Off of Africa...

23 Oct, 2025 13:45

Algeria inks $5.4 billion energy pact with Saudi M...

23 Oct, 2025 14:03