Energy Markets

Doha Strike Shakes Global Energy Assumptions

Israel’s September 9 military strike on Hamas leaders in Doha marked a shocking escalation of Middle East geopolitical conflict, threatening Qatar’s role as a diplomatic mediator and backbone of global energy security. The strike challenged Qatari sovereignty and the delicate balance of power in the region, especially following Israeli attacks on Iran. While immediate economic repercussions were contained, the strike introduces geopolitical risk that forces regional players, including Egypt, to critically re-evaluate their long-term energy strategies and security alliances.

Regional Turbulence, Global Ripples

This strike did not occur in isolation but represents the latest escalation in a region roiled by nearly two years of conflict following the Gaza war that erupted in October 2023, along with direct Israeli military strikes on Iran earlier this year. This ongoing turbulence is particularly alarming given the Middle East’s commanding position in global energy trade, with the region holding roughly 48% of the world’s proven oil reserves, according to GlobalData. Concerns about gas market implications have intensified, given that much of the region’s gas production comes from the South Pars/North Dome field—the world’s largest natural gas reservoir shared between Qatar and Iran.

A Subdued Market Response

The initial market reaction was sharp but brief, with Brent crude prices surging approximately 2% from around $66 per barrel to $67, while West Texas Intermediate (WTI) benchmarks climbed roughly 1.7% to reach $63 per barrel before both pared gains.

The increase occurred because Qatar is the world’s largest LNG exporter, and Gulf states and Iran collectively dominate global oil supply. Any tension holds theoretical potential to block oil flow through the Gulf, hindering shipments of up to 20 million barrels per day. However, this theoretical fear was immediately overwhelmed by current supply realities.

“Clearly, the strike has no oil infrastructure or shipment targets. It was a political assassination attempt, and markets shook off the risk quite quickly, as expected, following the result of the 12-day Iran–Israel war, which had little effect on oil as supply was never constrained,” Hamzeh Al Gaaod, Middle East and North Africa analyst at TS Lombard, told Egypt Oil & Gas.

The Muted Reaction Explained

The limited volatility poses a paradox: despite the strike occurring in a region housing the world’s largest oil and gas exporters—Qatar, Saudi Arabia, Iran, and others—the potential threat failed to trigger a sustained price shock. The answer lies in a complex interplay of factors, including Qatar’s immediate assurances that its energy infrastructure remained undamaged and operational, alongside global supply gluts, strategic OPEC+ decisions to increase production, and a market highly conditioned to regional risk. Nevertheless, concerns about the long-term reliability of Qatari LNG supplies and investment confidence have intensified among energy market participants and consuming nations.

OPEC+ decisions increased crude availability, offsetting risk premiums stemming from Middle East geopolitical tensions. The group raised output by 137,000 barrels per day (bbl/d) in October and maintained the same modest increase for November, while preserving oil market stability, according to an August 3 Egypt Oil & Gas report.

Global demand remains softer than expected, particularly in Europe. The region’s low growth rate and natural seasonal dip mean demand for both gas and oil is significantly reduced during summer and early fall. This weakness reduces urgency for major importers to panic-buy, allowing the market to absorb shocks.

Despite geopolitical turbulence, Qatar has provided assurances of continued LNG output to global markets, seeking to calm energy buyers and preserve its reputation as a reliable supplier.

Broader Regional, Global Implications

The Doha strike amplified concerns about potential flashpoints at critical maritime chokepoints, particularly the Strait of Hormuz, through which approximately 20 million bbl/d transit, according to the U.S. Energy Information Administration (eia). The attack on Qatar—viewed as a crucial anchor of European gas security—puts a direct geopolitical risk premium on a cornerstone of the continent’s new energy reality. Any conflict disrupting Gulf flows could push LNG prices up by at least 35%, according to Bloomberg Intelligence and Bloomberg Economics.

This incident lays bare profound energy vulnerability for Europe, whose post-Russian energy security is tightly tethered to geopolitical stability that is quickly eroding in the Gulf. Egypt’s position as an energy transit and processing hub makes it especially vulnerable to disruptions in regional energy flows, particularly given its reliance on Israeli gas supplies through the Eastern Mediterranean pipeline network.

However, Al Gaaod emphasized that actual supply risk remains limited. “There will always be a tail risk to Middle East supply while there is an ongoing conflict, but it is extremely minute,” he said. “You would need a genuine land invasion or threat to Iran to disrupt oil supply, as no other actor in the region—including Iran—has any interest in impacting supply through the Strait of Hormuz and beyond.”

Rethinking Energy and Security

The strike, though politically motivated rather than targeting energy infrastructure, forces European capitals to confront a strategic vulnerability: while its suppliers are diversified, exposure to geopolitical turbulence remains. This has reignited debate over accelerating the green transition, with the EU raising its 2030 renewable energy target to 42.5%.

The incident also shattered assumptions about American security guarantees for Gulf states, prompting a rethinking of regional security frameworks with implications for Egypt and the broader Middle East. It complicates further normalization between Israel and Arab states, as the Abraham Accords face renewed scrutiny following Israeli military action against an Arab capital.

When assessing the broader geopolitical landscape, Al Gaaod pointed to a different theater as posing a greater challenge. “Russia–Ukraine war poses a much bigger challenge to oil than any escalation in the Mid East,” he said. “Sanctions on Russia and Iran have essentially removed around 11 million bbl/d—nine million Russian, two million Iranian—from the market. Oil prices and the supply glut will depend on the geopolitical situation in that region, which is currently in escalatory rhetoric.”

Al Gaaod noted that market outlooks remain cautiously optimistic. “Should the geopolitical situation remain unchanged, we are slightly positive on oil and LNG due to bullish demand expectations on global growth next year,” he said.

The September 9 strike on Doha underscores the fragility of geopolitical stability in the world’s most critical energy-producing region. While markets demonstrated short-term resilience, the incident has permanently elevated risk premiums and accelerated strategic recalculations across consuming nations. Traditional security arrangements have proven insufficient to prevent regional escalation, forcing energy-importing nations to prioritize diversification, renewable investment, and genuine energy self-reliance as the only viable path to long-term energy security.

Related Articles

Renewable Energy Storage Market 2025 Forecast - La...

21 Oct, 2025 07:12

Solar power mistake in South Africa costs homeowne...

21 Oct, 2025 07:54

An Investor’s Guide to Africa...

21 Oct, 2025 09:47

GCC and Russia Deepening ties in a multipolar Midd...

23 Oct, 2025 11:59

Tesla prepares first steps into Africa with Morocc...

23 Oct, 2025 13:29

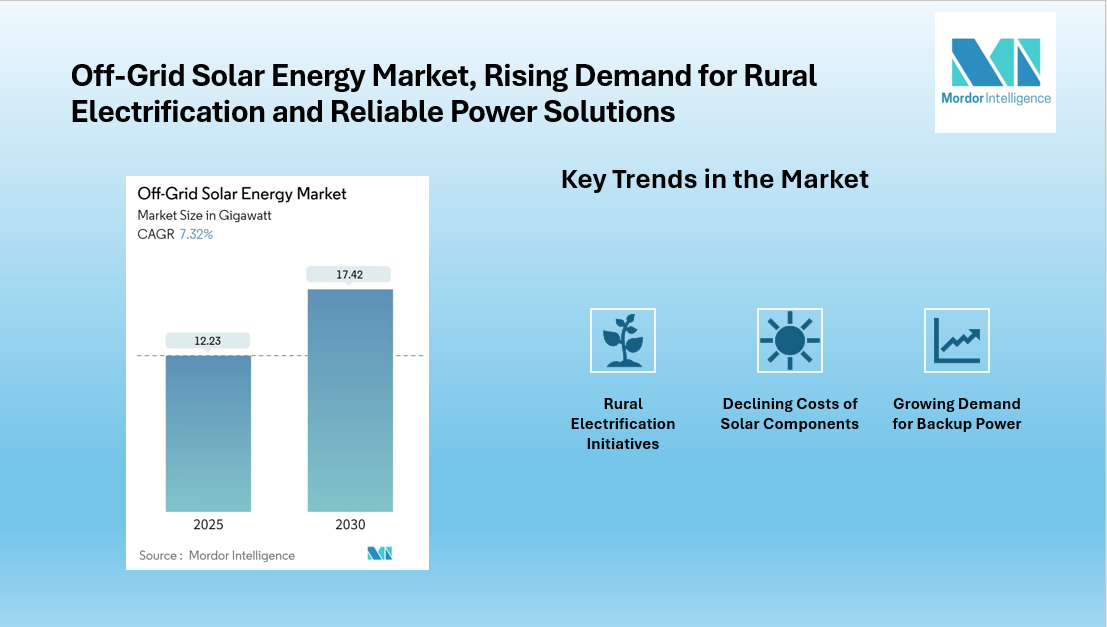

Off-Grid Solar Energy Market to grow at 17.42 GW b...

23 Oct, 2025 13:39

Petroleum Institute Urges Early Take Off of Africa...

23 Oct, 2025 13:45

Algeria inks $5.4 billion energy pact with Saudi M...

23 Oct, 2025 14:03

Middle East to pour $40 billion into upstream oil ...

27 Oct, 2025 08:09