Energy Markets

Oil prices slip 0.35 percent below $72 after OPEC+ approves another production increase

Oil prices slipped on Monday after OPEC+ approved another production increase beginning in August, while recovering exports through the Strait of Hormuz and stronger shipments from Russia reinforced expectations of improving global crude supplies.

Brent crude futures fell 0.35 percent to $71.87 per barrel, while U.S. West Texas Intermediate (WTI) crude declined 0.10 percent to $68.62 per barrel. WTI did not settle on Friday because U.S. markets were closed ahead of the Independence Day holiday.

Supply recovery weighs on crude prices

The modest decline follows several weeks of market focus on supply disruptions caused by the U.S.-Israeli conflict with Iran and uncertainty surrounding shipping through the Strait of Hormuz.

Investor sentiment has improved as oil exports from Gulf producers gradually recover and diplomatic efforts reduce fears of prolonged disruptions to one of the world’s most important energy trade routes.

Brent prices have now returned close to levels seen before the conflict despite production remaining below pre-war levels.

OPEC+ moves ahead with another production increase

On Sunday, OPEC+ agreed to raise production targets by an additional 188,000 barrels per day (bpd) from August, following identical increases approved for June and July.

The alliance continues its phased rollback of voluntary production cuts introduced in 2023.

However, much of the planned increase has yet to materialize because exports from key producers—including Saudi Arabia, Kuwait, and Iraq—were constrained after tanker traffic through the Strait of Hormuz was disrupted during the conflict with Iran.

The United Arab Emirates, which formally exited OPEC in May, has also continued increasing exports independently as regional production gradually normalizes.

Gulf exports rebound but remain below pre-war levels

Production and exports across the Gulf have shown significant improvement since the reopening of shipping routes.

According to a Reuters survey, OPEC oil production increased by 3.3 million bpd in June to 19.43 million bpd, recovering from its lowest level in more than two decades.

Meanwhile, Gulf crude exports rose by more than 3 million bpd from May to exceed 10 million bpd during June.

Despite the rebound, export volumes remain approximately 40 percent below levels recorded before the conflict, highlighting that supply normalization is still underway.

Russian exports add to global supply growth

Additional supply is also coming from Russia.

Crude shipments from the country’s western ports reached a record high in June and are expected to remain elevated through July after Ukrainian drone attacks damaged several domestic refineries, forcing more crude onto export markets.

The increase in Russian exports has added further downward pressure on prices by offsetting part of the supply losses experienced earlier this year.

Market watches pace of supply normalization

Oil traders continue to monitor the speed at which Middle Eastern production returns alongside developments in U.S.-Iran diplomacy and global demand trends.

While geopolitical risks remain present, improving export flows and rising production across several major exporters have shifted market attention back toward a more balanced supply outlook.

Oil prices remain under modest pressure as OPEC+ steadily restores production and exports from the Gulf recover following earlier disruptions. With additional barrels also entering the market from Russia, investors are increasingly focused on the pace of global supply normalization and whether demand will be strong enough to absorb the additional production in the months ahead.

Related Articles

Renewable Energy Storage Market 2025 Forecast - La...

21 Oct, 2025 07:12

Solar power mistake in South Africa costs homeowne...

21 Oct, 2025 07:54

An Investor’s Guide to Africa...

21 Oct, 2025 09:47

Doha Strike Shakes Global Energy Assumptions...

22 Oct, 2025 13:01

GCC and Russia Deepening ties in a multipolar Midd...

23 Oct, 2025 11:59

Tesla prepares first steps into Africa with Morocc...

23 Oct, 2025 13:29

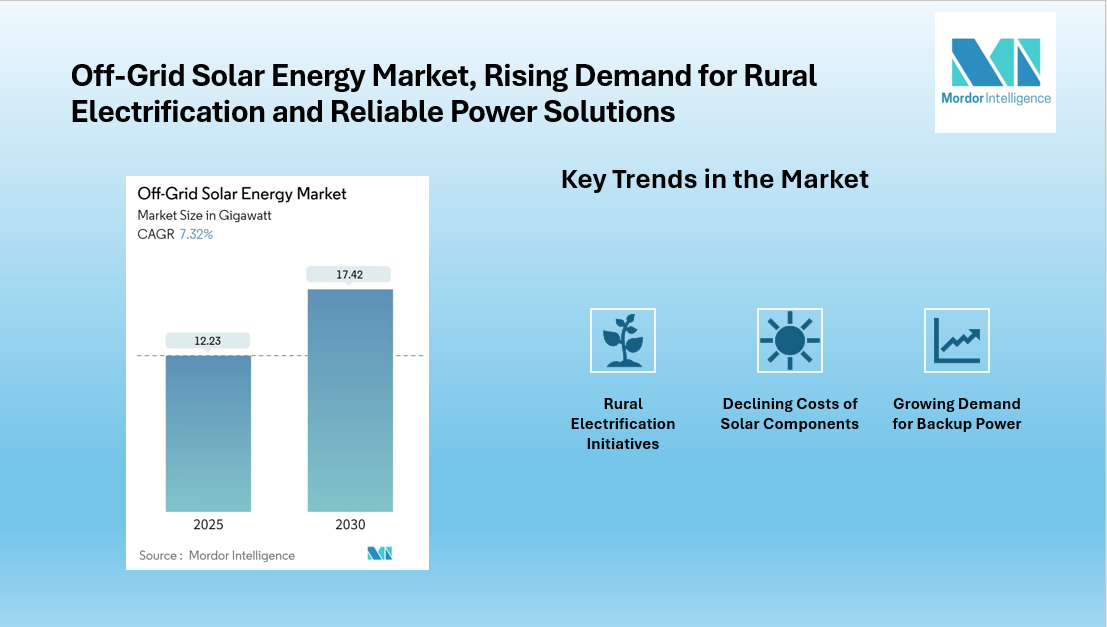

Off-Grid Solar Energy Market to grow at 17.42 GW b...

23 Oct, 2025 13:39

Petroleum Institute Urges Early Take Off of Africa...

23 Oct, 2025 13:45

Algeria inks $5.4 billion energy pact with Saudi M...

23 Oct, 2025 14:03