Energy Markets

Oil prices fall over 2 percent as Trump signals Middle East de-escalation

Oil prices fell more than 2 percent on Tuesday after U.S. President Donald Trump said he had paused plans to attack Iran with the aim of allowing negotiations to continue to end the war in the Middle East.

As of 5:09 GMT, Brent crude futures fell $2.32 or 2.07 percent to $109.8 a barrel, while U.S. West Texas Intermediate (WTI) crude fell $1.67 or 1.54 percent to $107 a barrel. In the previous trading session, both benchmarks climbed to their strongest levels since May 5 and April 30, respectively.

The June WTI contract is set to expire on Tuesday, while the more heavily traded July contract dropped $1.63, or 1.6 percent, to settle at $102.75 a barrel.

Reaction to de‑escalation efforts remains muted

Oil prices fell after Trump said on Monday that there was a very good chance Washington could secure a deal with Iran aimed at preventing Tehran from developing a nuclear weapon, shortly after announcing a pause in military operations to make room for negotiations.

Trump’s remarks reduced some short-term market concerns, but underlying risks remain. Investors are now assessing whether the comments indicate a real move toward de-escalation.

“Traders have become well accustomed to this cycle of weekend tension followed by Monday talk of progress. Consequently, the reaction to these de‑escalation efforts has been relatively muted compared to the early stages of the conflict,” said Tony Sycamore, Market Analyst, IG.

The ongoing Middle East conflict has effectively shut the Strait of Hormuz, a vital shipping route responsible for transporting roughly one-fifth of the world’s oil and liquefied natural gas supplies, fueling fears of major supply disruptions.

“The Middle East conflict has now dragged into its 12th week, and its influence continues to ripple with undeniable force across global markets. Persistent disruption to oil flows through the Strait of Hormuz has kept energy prices stubbornly elevated, feeding inflation fears, pushing up bond yields, and supporting a firmer United States dollar,” Sycamore added.

U.S. extends Russian sanction waiver

In a separate move, U.S. Treasury Secretary Scott Bessent prolonged a sanctions exemption for 30 days, enabling energy-vulnerable nations to keep importing Russian seaborne oil. The decision marked a reversal of the Treasury’s earlier stance against extending the waiver.

Several Asian nations, including major oil importers China and India, experienced supply disruptions due to the Iran conflict and turned back to Russian crude purchases to compensate for tightening Middle East supplies.

In the United States, a record 9.9 million barrels were withdrawn from the Strategic Petroleum Reserve last week, according to Energy Department figures, reducing inventories to roughly 374 million barrels, their lowest level since July 2024.

Related Articles

Renewable Energy Storage Market 2025 Forecast - La...

21 Oct, 2025 07:12

Solar power mistake in South Africa costs homeowne...

21 Oct, 2025 07:54

An Investor’s Guide to Africa...

21 Oct, 2025 09:47

Doha Strike Shakes Global Energy Assumptions...

22 Oct, 2025 13:01

GCC and Russia Deepening ties in a multipolar Midd...

23 Oct, 2025 11:59

Tesla prepares first steps into Africa with Morocc...

23 Oct, 2025 13:29

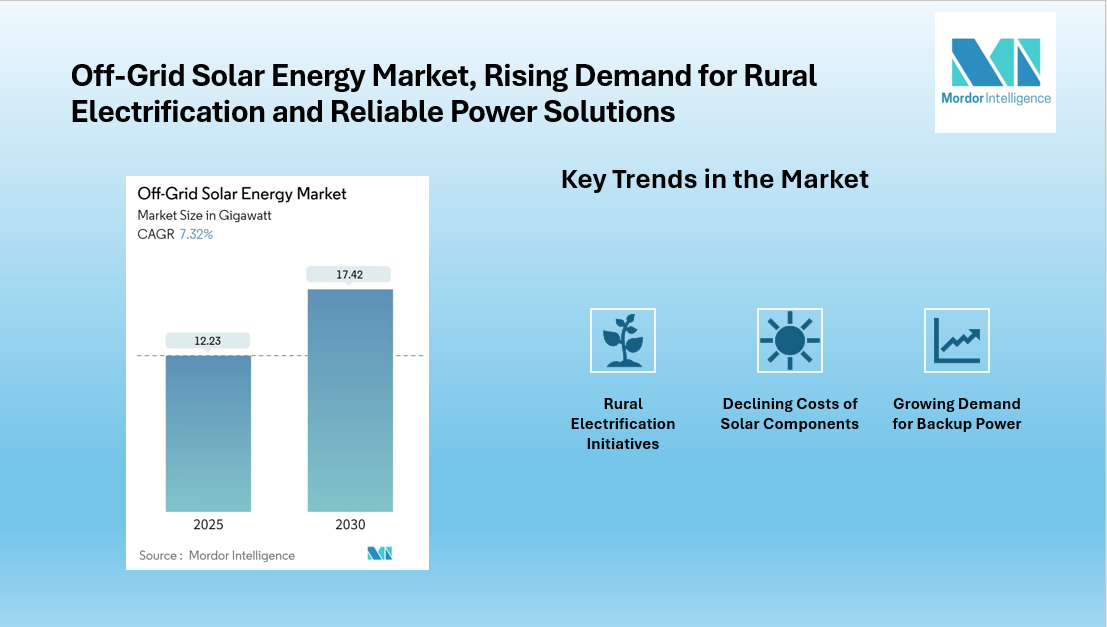

Off-Grid Solar Energy Market to grow at 17.42 GW b...

23 Oct, 2025 13:39

Petroleum Institute Urges Early Take Off of Africa...

23 Oct, 2025 13:45

Algeria inks $5.4 billion energy pact with Saudi M...

23 Oct, 2025 14:03