Energy Markets

Why energy markets cannot shake off the Middle East risk

The Muted Oil Market Response to Middle East Conflict

In June, a direct 12-day military clash between Iran and Israel, long feared as a nightmare scenario for global energy security, resulted in only a brief and modest fluctuation in oil prices. Despite the significant escalation, Gulf energy infrastructure remained unscathed, oil continued to flow, and a predicted 35% price surge never materialized. The price of Brent crude initially climbed 11% but soon fell below pre-conflict levels. This muted response stands in stark contrast to historical oil shocks, such as the 1973 embargo or the 1990 Iraqi invasion of Kuwait, which caused prices to double or quadruple. However, analysts caution against concluding that Middle Eastern instability no longer matters or that Gulf producers have lost their market leverage.

Factors Behind the Market's Resilience

The tempered market reaction can be attributed to a combination of short-term tactics and long-term structural shifts. In the immediate term, Israeli strikes targeted Iranian energy assets serving domestic consumption rather than critical export infrastructure. Furthermore, Iran’s calibrated retaliation, causing minimal damage, signaled a desire for de-escalation.

Structurally, several factors provided a buffer. Sluggish global oil demand, exacerbated by weak Chinese growth and US trade tariffs, created a soft market. Key Gulf producers had also pre-emptively raised output, contributing to a global oversupply. Over the past decade, these producers have invested in redundancy, developing alternative export routes like Saudi Arabia’s east-west pipeline and the UAE’s Habshan-Fujairah pipeline, which allow them to bypass the Strait of Hormuz. They also maintain large overseas storage facilities.

Finally, the global energy landscape has fundamentally changed. OPEC's share of global supply has declined from over 50% in the 1970s to around 33% today, diluted by the rise of new producers like the United States, Brazil, and Guyana. The US shale revolution, in particular, transformed the country from a major importer to a net exporter, altering global market dynamics.

The Paradox of Resilience and Enduring Vulnerabilities

Despite the recent calm, ongoing instability in the Middle East continues to pose a significant long-term risk to global energy markets. Strategic maritime chokepoints, such as the Strait of Hormuz and the Bab el-Mandeb, remain exposed to state and non-state threats. The fragile Iran-Israel ceasefire and the persistent threat of proxy attacks mean the risk of disruption to shipping lanes is a constant.

Furthermore, circumventing these chokepoints incurs costs. Longer alternative routes, like around the Cape of Good Hope, are more fuel-intensive and increase freight expenses. Predictions that the energy transition will swiftly negate the region's importance may also be premature. With peak oil demand not expected until at least 2030, global demand for liquid fuels will remain high for decades. As output from non-Gulf fields declines and US shale productivity wanes, the Gulf's role as the supplier of the cheapest and cleanest hydrocarbons is expected to be reinforced.

Strategic Imperatives for Europe

For Europe, the short-term market resilience should not be mistaken for lasting energy security. The continent remains exposed to Middle Eastern instability, as reducing dependence on its energy is complicated by geopolitical risks associated with other suppliers, including Russia and the United States.

European policymakers are advised to pursue a multi-pronged strategy. Investing in long-term stability through active diplomacy and supporting partners' maritime security capacities in the Gulf and Red Sea is essential. On the supply side, diversifying energy sources and accelerating the green transition under frameworks like REPowerEU are the best long-term defenses against geopolitical shocks. Deepening cooperation with Gulf states on energy security, crisis management, and clean technology, such as hydrogen, is also vital.

However, European policymakers face difficult trade-offs. Short-term diversification into fossil fuels from other regions risks locking in carbon-intensive infrastructure that conflicts with climate goals. Similarly, developing green hydrogen in North Africa for export could backfire if producing countries cannot meet their own energy needs. Integrating these elements into a cohesive strategy is crucial to balance energy security, climate objectives, and strong international partnerships.

Related Articles

Renewable Energy Storage Market 2025 Forecast - La...

21 Oct, 2025 07:12

Solar power mistake in South Africa costs homeowne...

21 Oct, 2025 07:54

An Investor’s Guide to Africa...

21 Oct, 2025 09:47

Doha Strike Shakes Global Energy Assumptions...

22 Oct, 2025 13:01

GCC and Russia Deepening ties in a multipolar Midd...

23 Oct, 2025 11:59

Tesla prepares first steps into Africa with Morocc...

23 Oct, 2025 13:29

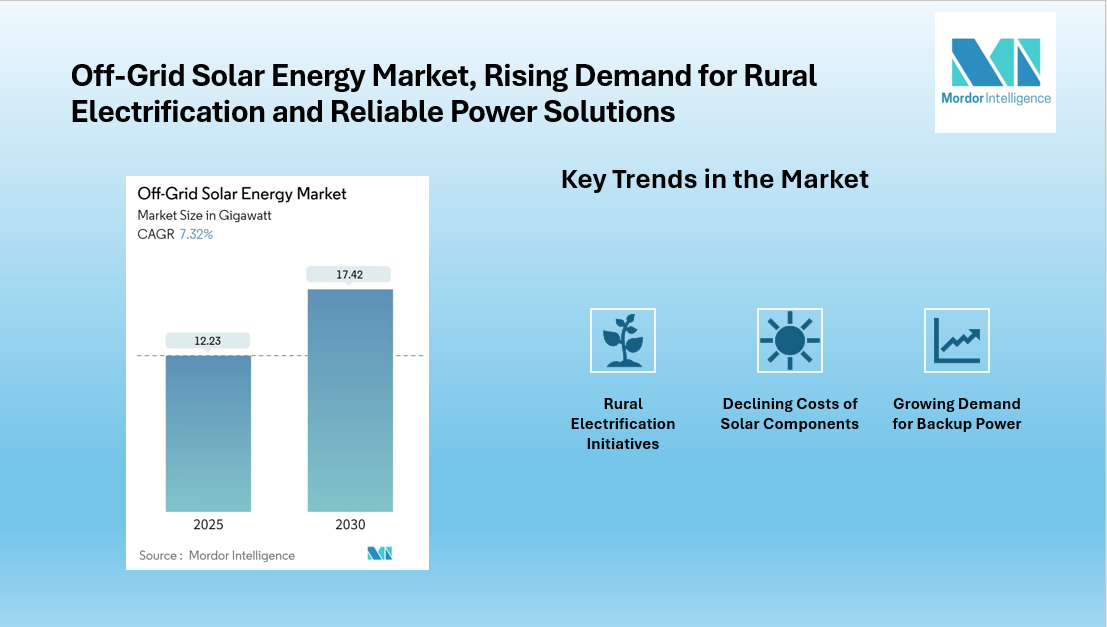

Off-Grid Solar Energy Market to grow at 17.42 GW b...

23 Oct, 2025 13:39

Petroleum Institute Urges Early Take Off of Africa...

23 Oct, 2025 13:45

Algeria inks $5.4 billion energy pact with Saudi M...

23 Oct, 2025 14:03