Energy Markets

Oil prices rise to $61.43 as Venezuelan crude disruptions, U.S. sanctions intensify market pressure

Oil prices climbed on Monday as escalating supply disruptions in Venezuela overshadowed persistent global surplus concerns. Brent crude remained steady at approximately $61.43 per barrel, an increase of 0.51 percent from Friday’s closing price. Meanwhile, West Texas Intermediate (WTI) rose by 0.52 percent, trading close to $57.54 per barrel, indicating a sense of cautious optimism in the trading sessions.

Venezuelan disruptions drive gains

Venezuela’s oil production plunged to multi-year lows, with output dropping to about 650,000 barrels per day (kbd) in November due to cascading failures at the José industrial complex. A fire at the Petrocedeno upgrader’s distillation unit, combined with prior closures of Petromonagas and Petrororaima units, left only the Petropiar unit operational, slashing heavy crude processing capacity by around 500,000 b/d. These outages, corroborated by flows averaging under 600 kbd this month, tightened heavy sour crude markets and buoyed differentials like Merey, which traded at a $12/bbl discount to ICE Brent.

U.S.-Venezuela tensions exacerbated the crisis, with new sanctions on shipping and a naval buildup under Operation Southern Spear curbing exports sharply. U.S. imports of Venezuelan crude fell to 130-150 kbd from a 300 kbd peak in December 2024, exposing firms like Chevron while raising fears of broader supply risks. Maritime data showed Venezuela’s exports declining post-seizures, supporting near-term price lifts despite Maduro’s overtures for U.S. investment deals.

Surplus projections temper rally

Global oil markets face a looming surplus, with OPEC+ pausing output hikes through Q1 2025 to navigate seasonal refinery maintenance and shield against downside. Forecasts predict a 260,000 b/d glut in 2025, ballooning to 1.01 million b/d in 2026 as non-OPEC supply outpaces demand growth of 1.21 million b/d. The EIA anticipates petroleum liquids supply rising 1.9 million b/d in 2025 and 1.6 million b/d in 2026, driven by shale and offshore projects.

IEA reports confirmed inventories at four-year highs, with Brent down 3 percent weekly and 18 percent yearly amid glut expectations. Non-OPEC+ gains, including from the U.S. and Brazil, are set to overwhelm sluggish OECD demand growth of 120,000 b/d, though India may lead non-OECD rises.

Russian crude under pressure

Russian crude faced headwinds from U.S. sanctions on Rosneft and Lukoil, with floating storage west of Suez surging to over 3 million barrels and exports to India potentially dipping post-November 21 deadline. India, averaging 1.89 million b/d Russian imports in November, eyes diversification to Middle East and U.S. sources, though workarounds like ship-to-ship transfers could limit impacts.

Kuwait ramped exports to 1.6 million b/d in November-December after Al Zour refinery outages, filling gaps for India and China. West African differentials strengthened on European cracks, despite Angola’s lower January loadings at 933 kbd, while Iranian flows to China lagged loadings due to quota exhaustion, building Asian floating storage.

U.S. market tightens slightly

U.S. crude stocks fell counter-seasonally last week on import drops to 1.8-1.9 million b/d and rising refinery demand, with offline capacity at 500 kbd. Baker Hughes noted a rig count decline, signaling caution amid high middle distillate cracks. Yet high domestic supply peaks this month cap upside, keeping WTI volatile around recent lows of $57.44.

Prices stabilized after December’s volatility—peaking at $63.93 on December 5 and dipping to $61.01 on December 11—but surplus threats loom large. Upside risks include escalated geopolitics or China demand beats; downsides from JP Morgan’s $30s Brent call by FY27 on non-OPEC surges. OPEC+’s steady quotas through March offer balance, but 2026 oversupply could pressure below $60.

Traders eye U.S. inventory data and Venezuela developments for direction, with Venezuelan woes providing tactical support against structural gluts.

Related Articles

Renewable Energy Storage Market 2025 Forecast - La...

21 Oct, 2025 07:12

Solar power mistake in South Africa costs homeowne...

21 Oct, 2025 07:54

An Investor’s Guide to Africa...

21 Oct, 2025 09:47

Doha Strike Shakes Global Energy Assumptions...

22 Oct, 2025 13:01

GCC and Russia Deepening ties in a multipolar Midd...

23 Oct, 2025 11:59

Tesla prepares first steps into Africa with Morocc...

23 Oct, 2025 13:29

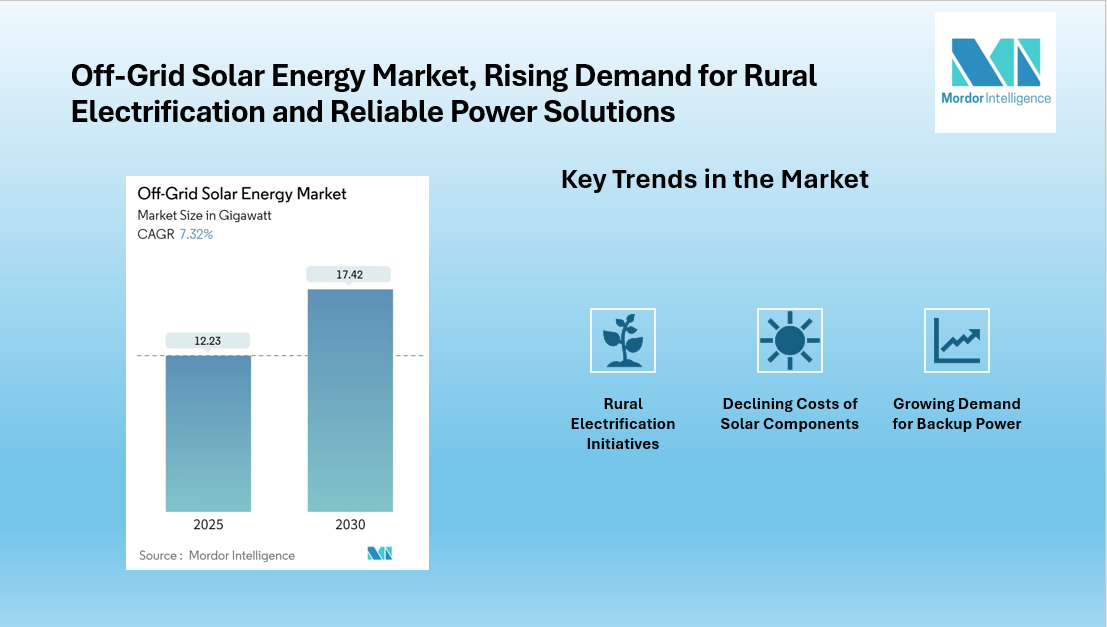

Off-Grid Solar Energy Market to grow at 17.42 GW b...

23 Oct, 2025 13:39

Petroleum Institute Urges Early Take Off of Africa...

23 Oct, 2025 13:45

Algeria inks $5.4 billion energy pact with Saudi M...

23 Oct, 2025 14:03