Energy Markets

Oil prices hover near two-week highs at $63.81 as markets await clarity from EIA, OPEC reports

Crude oil prices stabilized near two-week peaks on Monday, buoyed by expectations of a U.S. Federal Reserve interest rate cut and escalating geopolitical risks in key producing regions. Brent crude futures traded around $63.81 per barrel, up 0.09 percent on the day, while West Texas Intermediate (WTI) crude hovered near $60.16, reflecting a 0.13 percent gain. Despite year-to-date declines of over 11 percent, the benchmarks remained on track for weekly advances, underscoring a fragile balance between supply concerns and demand optimism.

Anticipation of a Fed rate reduction this week dominated trading sentiment, as lower borrowing costs could spur U.S. economic growth and lift fuel consumption in the world’s largest oil consumer. Markets priced in a high probability of a 25-basis-point cut, potentially easing recession fears and supporting industrial activity. Geopolitical premiums further bolstered prices, with stalled U.S.-Russia talks over Ukraine sustaining sanctions on Moscow’s energy exports and enabling ongoing Ukrainian strikes on Russian refineries and pipelines.

Tensions extended to Venezuela, where President Donald Trump’s signals of imminent action raised fears of disruptions to the country’s 1.1 million barrels per day (bpd) output, according to Rystad Energy estimates. Ukrainian attacks, including on the Druzhba pipeline, heightened supply risks without immediate flow interruptions, while Russian tanker activity surged amid U.S. sanctions. These factors offset softer elements, positioning oil for its first weekly rise in weeks.

Supply and demand pressures

Bearish counters capped upside potential. U.S. inventories rose by 574,000 barrels last week per EIA data, alongside gasoline and distillate builds, signaling ample stockpiles. Saudi Arabia slashed its January Arab Light crude price for Asia to a five-year low, reflecting weak regional demand, while Canadian heavy oil weakened. OPEC+ production hikes and surging non-OPEC output from the U.S., Brazil, and Canada fueled oversupply worries, with the IEA forecasting a market surplus next year.

Forecasts varied, with Trading Economics projecting Brent at $64.17 by quarter-end and $69.96 in 12 months, driven by macro models balancing risks. JP Morgan warned of a plunge to the $30s by FY27-end if non-OPEC supply outpaces demand, citing shale expansions and inventory builds.

Saudi price cuts signal tepid Asian demand

For Gulf Cooperation Council (GCC) producers, steady prices offered relief amid fiscal pressures, though Saudi price cuts highlighted Asia’s tepid appetite. OPEC+ ministerial talks reaffirmed gradual hikes of 400,000 bpd starting November, aiming to prevent gluts while responding to non-OPEC gains. Russia’s Urals crude traded at $54.92, down amid sanctions, underscoring Europe’s pivot from discounted barrels.

Broader energy markets mirrored caution: natural gas dipped 2.07 percent to $5.18, gasoline edged up 0.42 percent to $1.84, and heating oil held flat at $2.36. In India, retail petrol and diesel prices remained unchanged despite global fluctuations, unchanged since May 2022 per oil marketing companies. Traders eyed upcoming EIA and OPEC monthly reports for clarity on 2026 balances.

Volatility expected from Fed decisions and OPEC+ data

Volatility looms with the Fed decision, OPEC+ data, and Venezuela developments. Escalation in Ukraine or U.S. intervention could spike risk premiums, but robust supply growth—U.S. output at 13.844 million bpd, Saudi at 10 million bpd—poses downside threats. Analysts urged caution, noting overbought signals like Brent’s RSI above 77 in prior sessions.

Middle East stakeholders, from Riyadh to Abu Dhabi, navigate these dynamics amid energy transition pushes and AI-driven demand shifts in refining. Oil’s rebound, though modest, signals resilience against headwinds, with weekly closes potentially confirming bullish momentum.

Related Articles

Renewable Energy Storage Market 2025 Forecast - La...

21 Oct, 2025 07:12

Solar power mistake in South Africa costs homeowne...

21 Oct, 2025 07:54

An Investor’s Guide to Africa...

21 Oct, 2025 09:47

Doha Strike Shakes Global Energy Assumptions...

22 Oct, 2025 13:01

GCC and Russia Deepening ties in a multipolar Midd...

23 Oct, 2025 11:59

Tesla prepares first steps into Africa with Morocc...

23 Oct, 2025 13:29

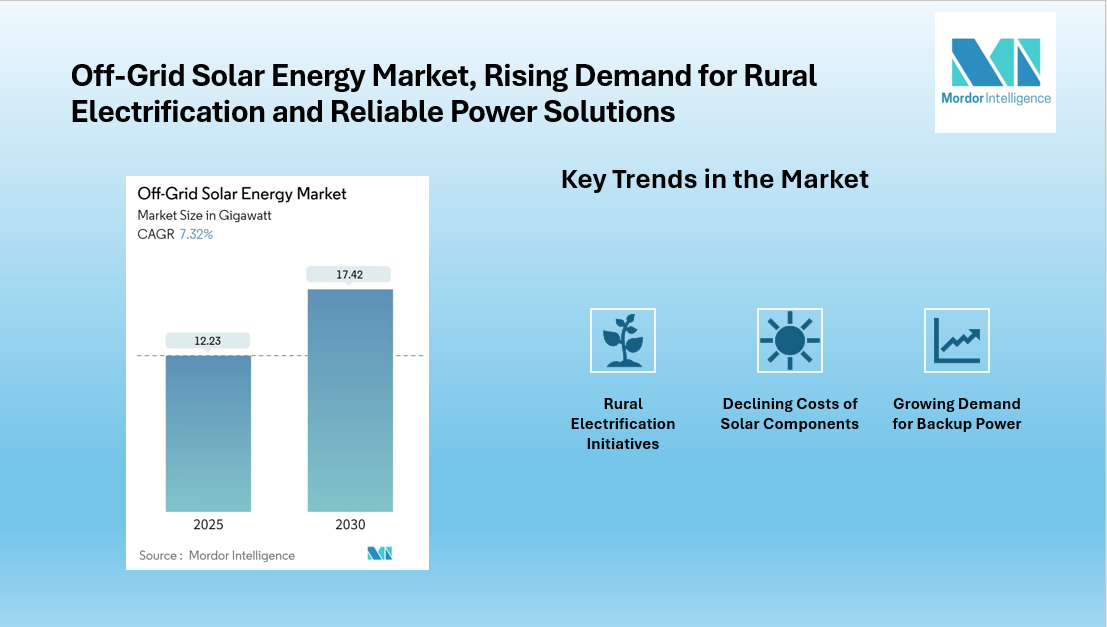

Off-Grid Solar Energy Market to grow at 17.42 GW b...

23 Oct, 2025 13:39

Petroleum Institute Urges Early Take Off of Africa...

23 Oct, 2025 13:45

Algeria inks $5.4 billion energy pact with Saudi M...

23 Oct, 2025 14:03