Base Metals

Zimbabwe mining investment rising steadily and extends beyond lithium

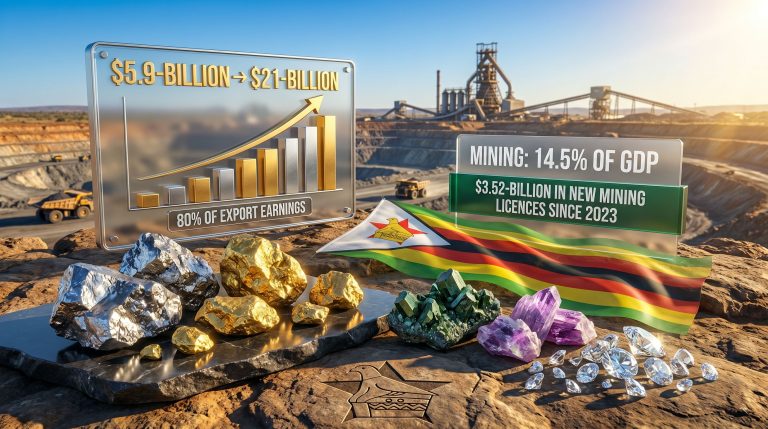

Since 2023, the Zimbabwe Investment and Development Centre has issued new mining licences worth $3.52-billion, while existing mining companies are undertaking massive expansion projects. For example, Zimplats, a unit of South Africa’s Impala Platinum, has invested more than $750-million in expansion, beneficiation, and energy projects, while Mimosa, another South African-owned platinum group metals (PGMs) miner, is investing more than $200-million.

Lithium Rush

Hogging the new investments are projects focused on lithium, a mineral crucial for battery manufacture – and therefore for the energy transition – that Zimbabwe has in abundance, with its current production accounting for 9% of global supply, according to London-based research and market analysis firm Benchmark Mineral Intelligence.

Most of the new lithium-sector investors are Chinese companies. Zhejiang Huayou Cobalt has been the biggest spender to date. Following its $422-million acquisition in April 2022 of Australian company Prospect Resources’ Arcadia lithium project, near Harare, it committed a further $300-million for a 400 000 t/y lithium concentrate plant, with production starting in 2023. It subsequently invested $400-million in a 50 000 t/y plant producing lithium sulphate – an intermediate battery material used in the production of lithium hydroxide and lithium carbonate – which was completed in 2025.

Other Chinese companies active in the Zimbabwean lithium sector include Sinomine Resources Group, Chengxin Lithium Group and Yahua. Sinomine acquired the old Bikita lithium mine for $180-million in January 2022 and had spent an additional $300- million to expand mining operations and build a spodumene concentrate plant by mid-2023, announcing in October 2024 it planned to build a $500-million smelter over the next five years.

Meanwhile, Chengxin Lithium Group and fellow Chinese enterprise Canmax Technologies paid $77-million for the Sabi Star mine in 2021 before investing $130-million to develop the mine and build a concentrator, a project that was completed in 2023.

Yahua announced in February 2026 that it planned to build a lithium sulphate plant at the Kamativi mine, which it runs in a joint venture with the Zimbabwean State.

In July 2024, Zimbabwe’s State-owned Kuvimba Mining House announced that it had signed a $310-million deal with a consortium of unnamed Chinese and British investors for the construction of a lithium concentrator at the Sandawana mine.

Explaining Zimbabwe’s appeal to foreign lithium investors, Benchmark lithium product director Cameron Perks points to the country’s substantial reserves, available skills, given its exploration and mining history, and relative policy stability, which, however, has changed somewhat following the sudden stoppage of all exports and the imposition of higher royalties.

Beyond lithium, foreign investors have invested substantially in gold and PGMs projects. In the PGMs sector, JSE- and London Stock Exchange-listed Tharisa plc has, through its Karo Mining subsidiary, spent $241-million to date on developing the Karo mine, 85 km south-west of Harare.

Commenting on whether the investment experience in Zimbabwe matched expectations when the Karo project was first announced, a senior Tharisa executive said: “When measured on a capital-intensity-per-ounce-of-production basis, we are tracking well, bearing in mind that the majority of the infrastructure has to be built for the initial ten years that has been planned, but we have significant upside of an additional 50 years of production, so this will be amortised over a long period.”

He does not have any concerns about Zimbabwe’s mining investment climate, stating: “We see Karo and the Zimbabwe jurisdiction very much in line with our Tharisa mine [in South Africa] in terms of development and executability. Skills in Zimbabwe and technical knowledge and experience are extremely high.”

Reflecting Tharisa’s belief that it should have control of the entire value chain, the company plans to spend more millions in Zimbabwe, replicating its model at Tharisa mine, where it has pursued downstream opportunities over time.

Policy Questions

For Benchmark’s Perks, what he describes as opaque royalty and tax structures, alongside policy unpredictability, are a cause for concern for potential investors. Commenting specifically on the burgeoning lithium sector, he urges the Zimbabwean government to invest in infrastructure, commit to policy stability and consider being flexible on the in-country downstream requirement for lithium companies.

“Zimbabwe was already exporting lithium concentrate, a value-added material. It now wants to encourage chemical production. It can be done, and we have seen lithium sulphate produced, but it is yet to be seen if it will provide economic benefits, especially since it is cheaper to do this level of value-add in China itself,” he tells Engineering News & Mining Weekly.

“Australia still receives massive economic benefit from mining and shipping [lithium concentrate]. Arguably, the chemical production it has participated in so far has been a net negative.”

Zimbabwe has for decades been the subject of negative media coverage – from the early 2000s, when the Mugabe administration seized white-owned farmland for redistribution to landless blacks to multiple disputed elections and the ongoing controversy around an attempt to extend by two years the current terms of the President and Parliament beyond their constitutional end in 2028.

Still, Perks insists that, in the context of lithium-bearing countries, Zimbabwe’s business environment “is above the African average”. However, in general terms, South Africa and Namibia “appear to be safer for now”.

Gift Mugano, an economics professor and executive director of Africa Economic Development Strategies, a Harare-based think-tank, is also optimistic about the prospects of the Zimbabwean mining sector, which accounts for 14.5% of GDP, generates about 80% of export earnings, contributes close to 19% of government revenue and continued to anchor economic growth in the first quarter of 2026, supported by high gold, PGM and lithium prices.

In 2025, the sector grew by 7% on the back of investments over the past few years, with 10% growth projected this year. Further, mineral export revenue is estimated to have increased from $5.9-billion in 2024 to $6.2-billion in 2025, with projections indicating eventual growth to $21-billion if ongoing projects are successfully completed.

Mugano’s optimism is reinforced by the fact that, while policy inconsistency and instability constrained Zimbabwe’s business environment between 2000 and 2017, recent reforms have been a key factor behind the mining sector’s resurgence. They include a reduction in licence processing times from 21 days to only seven days, which he says has improved investor confidence, as indicated by the surge in mining-sector investment.

However, he hastens to add that royalty increases, foreign currency retention policies, and a lack of clarity on black empowerment rules continue to concern foreign investors.

Like Perks, he also flags energy and infrastructure deficits as potential impediments to continued foreign mining investment flow.

“Findings from the State of the Mining Sector Survey show that electricity demand increased by approximately 20% in 2024 due to expansion projects, and in the same year diesel consumption rose by 35%, reflecting efforts to compensate for unreliable grid power.

“Most mining executives expect power shortages to worsen as new projects come online. Without reliable electricity, beneficiation, smelting and processing projects cannot operate efficiently.

“In addition, due to the absence of a well-functioning railway system, transport infrastructure remains a significant bottleneck, increasing production costs and reducing competitiveness.

“Further, while Zimbabwe retains a relatively strong mining skills base, future expansion in lithium processing, metallurgy and advanced mining technologies will require additional technical expertise.”

Industrial Promise

In a thumbs up for the Zimbabwean government’s push for in-country mineral beneficiation, Mugano says moving downstream could see the mining sector become the cornerstone of Zimbabwe’s industrialisation strategy. He believes that the strongest opportunities are in lithium processing, platinum refining, ferrochrome production, gold refining and jewellery manufacturing.

Further enhancing mining’s potential contribution to industrialisation, according to Mugano, is the Zimbabwean government’s promotion of the Mines-to-Energy Park, which includes two 300 MW power stations, a lithium salt plant producing 130 000 t/y, graphite processing facilities, a nickel sulphide production facility and an alloy smelting facility.

“Countries such as Botswana, Australia, Chile, and Indonesia provide useful examples of how mineral wealth can support industrialisation through beneficiation, local supplier development and infrastructure investment,” says Mugano.

Asked what he would single out as the factors to watch most closely if he were advising a global mining investor considering Zimbabwe, he said: “With over 60 minerals, including precious minerals, base metals and rare-earth minerals, Zimbabwe offers one of Africa’s most compelling mining opportunities in the world.

“In line with the government policy on mineral beneficiation across all categories of minerals, investors should watch developments, but must place emphasis on the call by the government of Zimbabwe on the need to establish processing facilities in iron and steel, gold, lithium and platinum group metals, as well as Mines-to-Energy projects.”

Even if mining foreign direct investment continues to pour into Zimbabwe, Mugano argues that the ultimate measure of success will be the sector’s contribution to broad-based economic development. For him, a successful mining sector is one that increases mineral export revenue to more than $21-billion a year, creates 100 000 mining jobs and many more in linked manufacturing and service sectors over the next five years, contributes more to GDP than the current 12% to 14.5%, has a stronger fiscal revenue contribution and raises local procurement beyond the current 15%.

“Success would also mean mining becomes the foundation of industrialisation rather than simply an export sector. A disappointing outcome would be one where Zimbabwe continues exporting mainly raw minerals, while importing higher-value manufactured products.”

Related Articles

Sanu Gold Announces $5 Million Private Placement L...

06 Sep, 2024 13:08

Ivanhoe Mines produces 40,347 tonnes of copper at ...

09 Sep, 2024 09:21

Andrada partners with SQM to develop Namibia lithi...

10 Sep, 2024 08:56

US, Saudi Arabia in talks to secure metals in Afri...

10 Sep, 2024 09:07

DRC: Eurasian Secures $150 Million to Develop a Co...

12 Sep, 2024 06:22

Zambian mines desperate for power turn to a surpri...

13 Sep, 2024 11:18

Africa at the cusp of a critical minerals boom...

17 Sep, 2024 07:40

Coolabah to unite Broken Hill assets, paving path ...

17 Sep, 2024 08:40

Marula Mining completes first manganese exports sa...

18 Sep, 2024 09:05